Tariff Tuesday: What’s Next?

If you're new to this newsletter, I share my thoughts on markets, careers, and wealth-building. Welcome aboard!

Duration mismatch is like when one person is dating to marry and the other is stringing together one-night stands.

I remember vividly joining Farmer's Insurance on the bond desk in 1994.

These “genius” bond investors had purchased IO and PO bonds, Interest Only and Principal Only. They were high-yield and guaranteed. Nothing could go wrong as long as interest rates stayed nice and steady.

This was a mini-2008 financial crisis, but in 1994. They lost their shirts because the bonds they invested in to pay for Farmer's insurance claims moved at different rates than the claims they were supposed to be covering when interest rates jumped around. It was a disaster.

Today may be another duration mismatch.

Longer-term, making government spending less of a burden on all of us is a good thing. It should lead to lower taxes and thus a higher standard of living for most of us. All sounds good so far. This is why stocks rallied strongly into the Trump presidency.

But in my November 2024 letter, I warned of the second shoe to drop.

Those very longer-term benefits of lower government spending have near-term negative repercussions as they work their way through our economy, or GDP = C + I + G + (X-M)

Before we reach the longer-term hopeful nirvana of lower government spending and lower taxes, we are faced with our short-term reality:

Massive firings and shutdowns of entire government agencies

Unemployed government workers cutting their own spending as consumers

Freezing of government budgets that represent revenues for many large US companies

Large US companies facing revenue uncertainty, cutting their budgets and forecasts

Stock markets never react well to decreased forecasts and lack of visibility

Tariffs are likely to lead to increased prices in an already inflationary environment, pressuring consumers

Inflation not giving the Fed room to cut interest rates, even if we see a slowing of the economy.

In the classic duration mismatch, we could see inflation go higher with tariffs, causing interest rates to stay higher, thereby increasing the chances of recession.

Recession is an antidote for inflation because demand decreases which puts downward pressure on prices. But you have to be in the recession to get this benefit. Recessions come at a large cost in terms of job losses, stock market declines, and general hardship.

Tariffs could tie the Fed's hands by driving up inflation, thus not allowing the Fed to reduce interest rates to support the economy.

More recession warnings have started flashing recently, with the number one leading indicator being the stock market itself.

No matter how you feel about Trump, I do understand the urgency with which he is pushing Musk to get this done. The longer the uncertainty lasts and the slower they cut costs, the worse it will be for the markets and the economy.

On November 23, 2024 I wrote about what the economy and stock market might do under a Trump presidency.

Here's a quick review of what makes up the economy, or GDP = C + I + G + (X-M)

C = Consumer spending, 68% of GDP in 2023, average 63-68%

I = Business Investment, 18%, average 13%, range 11-15%

G = Government Spending, 17%, range 18-22%, but 2020-1: 43-45%

X - M = Exports minus Imports, -3% (a trade deficit).

Elon Musk recently tried to explain the needle we are trying to thread:

“If the economy grows faster than the money supply and we stop government waste, then we can reduce inflation, reduce interest rates, and increase everyone's standard of living.”

This is Goldilocks and the 3 bears scenario. Not too hot. Not too cold.

But the economy is big and complex, even if I can boil it down to a relatively simple formula above, that doesn't mean it is simple to control.

The rates of growth of each variable are hard to control. Furthermore, I took an entire econometrics class on the interaction between the variables (i.e. they are not independent variables, but often increases in one lead to changes in another), which makes the whole thing nearly impossible to control. It's like controlling a puppet that has strings running to another nearby puppet which has a different person controlling those strings.

Example of variables that interact?

DOGE is reducing government spending G. That might reduce GDP unless other areas grow. But the government is a big spender with consulting firms and other companies, to the tune of 20% or more of their revenues. Many of those firms have seen a freezing of government budgets.

Often the government decision-maker has been fired.

So at the very least, the deal, or revenue, will be delayed until it is reviewed by a new person. Companies that all of a sudden see 20% of their revenue frozen must react by freezing parts of their spending ("I" or Investment in the above formula). So G goes down and I goes down, leading to a double-negative in GDP, or economic growth.

And the worst possible outcome?

We've seen investigative reporters showing the savings aren't nearly as much as advertised because of double and triple counting of budget line items.

The government is indeed a sprawling entity, very different from the centralized model of Twitter where Musk summarily fired 80% of the workers in a matter of months.

Here it's time-consuming to find the programs, cancel them, find the people, and fire them, bit by bit.

Thus, we are getting all the uncertainty the market hates, lots of frozen budgets, and negative impacts on corporations who sell to the federal government, WITHOUT the benefits of the large and rapid savings.

Reducing “G” or government spending will take time, but the fear and paralysis are immediate, and the ripple effects are negatively impacting the economy.

Some speculate that spending won't be cut dramatically, but instead, Musk will make noise, fire people, and create chaos to make it look like they are doing something dramatic as a cover for the huge tax cuts being put in place for corporations and the wealthy. Hard to say…

Either way, markets hate uncertainty, and this type of uncertainty is causing real budget and program freezes, which is hurting earnings and the economy.

Could tariffs help with GDP by reducing our trade deficit?

Some say quite simply that tariffs are a tax. We'll dive deeper.

Let's look at the formula again. GDP = C + I + G + (X-M)

And right away, that pesky two-variable interaction comes into play. If we put a 25% tariff on alcohol from Canada, the consumer either pays 25% more, and has to cut their budget elsewhere, or buys less from Canada. My guess is some of the tariff is passed on through higher prices and some of the burden is borne by the Canadian companies through lower profit margins (Canada's GDP will decrease because companies can't invest as much with lower profit margins).

Back to the US.

Consumers facing higher prices to the tune of 15-20% (with exporters to the US swallowing part of the tariff in lower profits) are likely to budget for that by buying less. Perhaps “C” stays at the same or higher level, but it is through higher prices, not through increasing consumption, or getting more, i.e. a higher standard of living is not achieved even though GDP grows.

Canada's biggest exports to the US in dollar size are crude oil, natural gas, and machinery and equipment manufacturing, including automotive and parts.

This means the 25% tariff, i.e. price increase, will be hitting our US car manufacturers who use Canadian parts. This will put downward pressure on US car companies' margins, and also increase the likelihood they will need to raise prices to consumers, who are likely to cut back spending on the margin, "C" and these auto companies will then have less money to invest “I”.

There's a reason these are called tariff wars and not just tariffs. I have covered a few examples of what happens when the US imposes 25% tariffs on Canada. But Canada will respond in kind, raising prices for all US goods entering Canada, and wreaking the same havoc on their consumer prices, supply chains, and economy.

Canada's focus with their first tariff announcement appears to be hurting US farmers and rural economies, both strongholds of Trump supporters, by increasing tariffs on fertilizer.

In 2023, Canada produced 32.4% of the world's potash, making it the world's largest producer. Canada also has the largest potash reserves in the world. Potash is a potassium-rich fertilizer that helps plants grow, increases crop yields, and improves water retention. It's a key plant nutrient that's essential for the agricultural industry.

This is a day-by-day story, with Trump already carving out tariffs on agriculture in the hopes that Canada reciprocates to spare US farmers. Trump also gave automakers a 30-day reprieve.

China is an even bigger story, with far larger supply chain implications. After decades of outsourcing our manufacturing to China (and enjoying higher profit margins and lower consumer prices from that outsourcing activity), China now sends us nearly 5X the goods that we send them. A massive trade imbalance.

What does China send us?

Putting tariffs on Chinese imports will do the same thing as any tariffs on imports: it will immediately raise prices of various consumer items as well as supply chain components of popular electronic goods, including the iPhone.

No matter which way you slice it, having tariffs complicates supply chains, pricing, and forecasting. The daily back-and-forth creates a deer in headlights, frozen behavior from company leaders who need time to plan, shift, and act on behalf of their large companies. And markets don't like uncertainty.

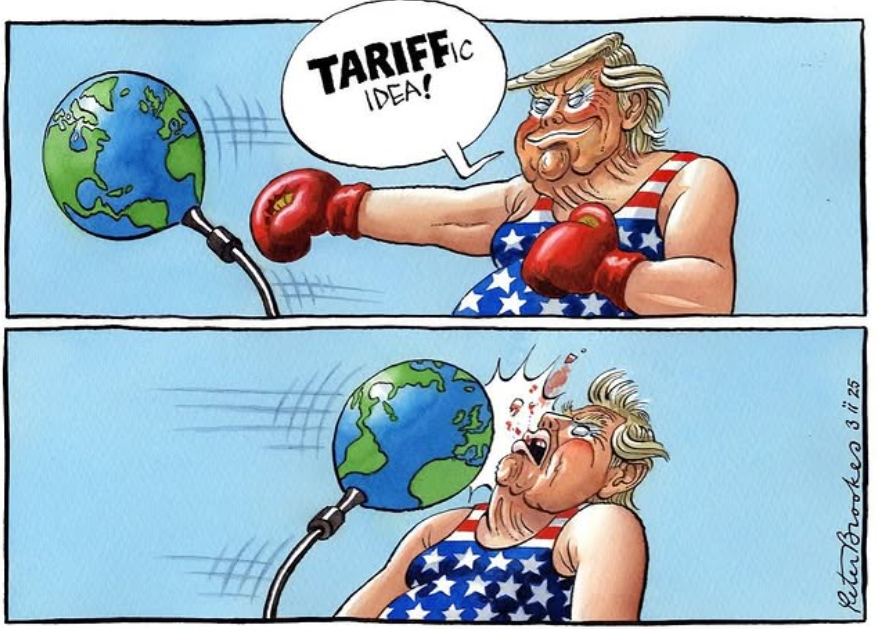

Bottom line, tariffs drive up prices, which is inflationary, and daily changes in tariff policies create inaction which slows growth.

The second variable that's impacted in GDP? (X-M)

In general, we are a net importer (although, funnily enough, our trade deficit with Canada is nearly balanced, unlike China and Mexico). BMWs, Mercedes, iPhones made in China, etc. One goal Trump has, which in itself may be a noble goal, is to be less of a net importer. If we exported more and imported less, that would mean X-M would be a bigger number, thus GDP would be a bigger number. It is good for growth.

However, consumers want what we want.

Are people going to turn in their BMWs for Fords because of a tariff? Probably not. On the margin, they may wait a bit longer for what they want, putting a damper on demand.

If you look at the extremes, there are 5-year waiting lists for a Hermes purse, and most of the time you have to spend $100K on other items before being offered the “opportunity” to get on the list to buy a purse for $10K.

Rolex prices have come down from their peak, but you still can't even get on a waiting list for a new one in a popular model. No one is switching to a US-made watch because Rolex is sold out. It makes them want it more.

So on X-M, M (imports) goes UP through tariffs being added to what people want. Perhaps people delay the purchase, but on the margin, M goes UP. Maybe over time, people learn to love US goods more and find substitutes, but over the shorter term, we will likely see some combination of paying more and delaying purchases.

This is another example of duration mismatch wherein tariffs take too long to train people to change their preferences to US goods, if they ever could. Often higher prices drive people to want something even more.

My guess is with the easy credit situation, we will see people simply pay more for the imports they want. That's inflation, pure and simple.

Inflation means the Fed has to keep interest rates higher for longer, which starts making Musk's statement fall apart.

Maybe it seemed simpler to drive economic growth in the past because in the last decade, we saw lower interest rates (the cost of money) leading to increases in investing, lending, and borrowing. That led to nominal growth in the economy. But those lower interest rates that stayed low for too long led to inflation of everything we buy, including real estate and stocks.

Right now, there are a lot of variables interacting with each other. If we go back to Musk's statement:

“If the economy grows faster than the money supply and we stop government waste, then we can reduce inflation, reduce interest rates, and increase everyone's standard of living.”

I think it's a bit of wishful thinking that we will get through all of this without any (economic) bumps in the road. We're more likely to experience this cycle's version of duration mismatch.